Austerity has failed. It turned a nascent recovery into stagnation. That imposes huge and unnecessary costs, not just in the short run, but also in the long term: the costs of investments unmade, of businesses not started, of skills atrophied, and of hopes destroyed.

What is being done here in the UK and also in much of the eurozone is worse than a crime, it is a blunder. If policymakers listened to the arguments put forward by our opponents, the picture, already dark, would become still darker.

How Austerity Aborted Recovery

Austerity came to Europe in the first half of 2010, with the Greek crisis, the coalition government in the UK, and above all, in June of that year, the Toronto summit of the group of twenty leading countries. This meeting prematurely reversed the successful stimulus launched at the previous summits and declared, roundly, that “advanced economies have committed to fiscal plans that will at least halve deficits by 2013.”

This was clearly an attempt at austerity, which I define as a reduction in the structural, or cyclically adjusted, fiscal balance—i.e., the budget deficit or surplus that would exist after adjustments are made for the ups and downs of the business cycle. It was an attempt prematurely and unwisely made. The cuts in these structural deficits, a mix of tax increases and government spending cuts between 2010 and 2013, will be around 11.8 percent of potential GDP in Greece, 6.1 percent in Portugal, 3.5 percent in Spain, and 3.4 percent in Italy. One might argue that these countries have had little choice. But the UK did, yet its cut in the structural deficit over these three years will be 4.3 percent of GDP.

What was the consequence? In a word, “dire.”

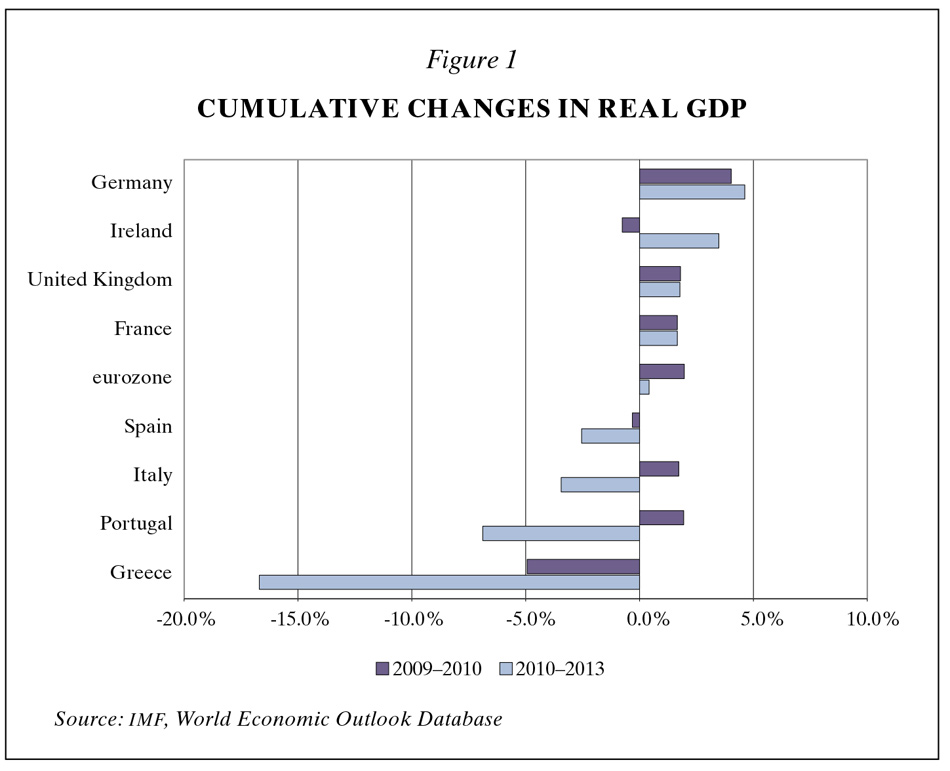

In 2010, as a result of heroic interventions by the monetary and fiscal authorities, many countries hit by the crisis enjoyed surprisingly good recoveries from the “great recession” of 2008–2009. This then stopped (see figure 1). The International Monetary Fund now thinks, perhaps optimistically, that the British economy will expand by 1.8 percent between 2010 and 2013. But it expanded by 1.8 percent between 2009 and 2010 alone. The economy has now stagnated for almost three years. Even if the IMF is right about a recovery this year, it will be 2015 before the economy reaches the size it was before the crisis began.

The picture in the eurozone is worse: its economy expanded by 2 percent between 2009 and 2010. It is now forecast to expand by a mere 0.4 percent between 2010 and 2013. Austerity has put the crisis-hit countries through a wringer, with huge and ongoing recessions. Rates of unemployment are more than a quarter of the labor force in Greece and Spain (see figure 2).

When the economies of many neighboring countries contract simultaneously, the impact is far worse since one country’s reduced spending on imports is another country’s reduced export demand. This is why the concerted decision to retrench was a huge mistake. It aborted the recovery, undermining confidence in our economy and causing long-term damage.

Why Fiscal Policy

Why is strong fiscal support needed after a financial crisis? The answer for the crisis of recent years is that, with the credit system damaged and asset prices falling, short-term interest rates quickly fell to the lower boundary—that is, they were cut to nearly zero. Today, the highest interest rate offered by any of the four most important central banks is half a percent. Used in conjunction with monetary policy, aggressive and well-designed fiscal stimulus is the most effective response to the huge decrease in spending by individuals as they try to save money in order to pay down debt. This desire for higher savings is the salient characteristic of the post–financial crisis economy, which now characterizes the US, Europe, and Japan. Together these three still make up more than 50 percent of the world economy.

Of course, some think that neither monetary nor fiscal policy should be used. Instead, they argue, we should “liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate.” In other words, sell everything until they reach a rock-bottom price at which point, supposedly, the economy will readjust and spending and investing will resume. That, according to Herbert Hoover, was the advice he received from Andrew Mellon, the Treasury secretary, as America plunged into the Great Depression. Mellon thought government should do nothing. This advice manages to be both stupid and wicked. Stupid, because following it would almost certainly lead to a depression across the advanced world. Wicked, because of the misery that would follow.

Austerity in the Eurozone

Some will insist that the eurozone countries had no alternative: they had to retrench.

This is true in the sense that members have limited sovereignty, wed as they are to a single currency, and had to adapt to the dysfunctional eurozone policy regime. Yet it did not have to be this way.

Advertisement

1. The creditor countries, particularly Germany, could have recognized that they were enjoying incredibly low interest rates on their own public debt partly because of the crises in the vulnerable countries. They could have shared some of this windfall they enjoyed with those under pressure.

2. The needed adjustment could have been made far more symmetrical, with strong action in creditor countries to expand demand.

3. The European Central Bank could have offered two years earlier the kind of open-ended support for debt of hard-pressed countries that it made available in the summer of 2012.

4. The funds made available to cushion the crisis could have been substantially larger.

5. The emphasis could then have been more on structural reforms, such as easing labor regulations and union protections that restrain hiring and firing and raise labor costs, and less on fiscal retrenchment in the form of reduced spending. Reduced labor costs could have made these nations’ export industries more competitive and encouraged domestic hiring.

It is possible to admit all this and yet argue that without deep slumps, the necessary pressure for adjustment in labor costs that is inherent in the adoption of a single currency (which is a modern version of the gold-standard-type mechanism that once ruled the advanced nations and helped bring on the Great Depression) would not have existed.

This, too, is in general not true.

1. In Greece, Ireland, Portugal, and Spain, at least, the private sector was in such a deep crisis that additional downward pressure as a result of rapid fiscal retrenchment simply added insult—and more unemployment—to deep injury.

2. In Italy, the pressure from years of semi-stagnation, with many more to come, would probably have been sufficient to restructure the labor markets, to bring about lower labor costs, provided structural reforms of the labor market were carried out, measures allowing companies to reduce their workforces and adjust wages more easily.

In short, the scale of the austerity was unnecessary and ill-timed. This is now widely admitted.

Austerity in the UK

The UK certainly did have alternatives—a host of them. It could have chosen from a wide range of different fiscal policies. The government could, for example, have:

1. Increased public investment, rather than halving it (initially decided by Labour), when it enjoyed zero real interest rates on long-term borrowing.

2. It could have cut taxes.

3. It could have slowed the pace of reduction in current spending.

It could, in brief, have preserved more freedom to respond to the exceptional circumstances it confronted.

Why did the government not do so?

1. It believed, and was advised to believe, that monetary policy alone could do the job. But monetary policy is hard to calibrate when interest rates are already so low (at or close to zero) and potentially damaging particularly in the form of asset bubbles. Fiscal policy is not only more direct, but it can also be more easily calibrated and, when the time comes, more easily reversed.

2. The government believed that its fiscal plans gave it credibility and so would deliver lower long-term interest rates. But what determines long-term interest rates for a sovereign country with a floating exchange rate is the expected future short-term interest rates. These rates are determined by the state of the economy, not that of the public finances. In the emergency budget of June 2010, the cumulative net borrowing of the public sector between 2011 and 2015–2016 had been forecast to be £322 billion; in the June 2013 budget, this borrowing is forecast at £539.4 billion, that is, 68 percent more. Has this failure destroyed confidence and so raised long-term interest rates on government bonds? No.

3. It believed that high government deficits would crowd out private spending—that is, the need of the government to borrow would leave less room for private borrowing. But after a huge financial crisis, there is no such crowding out because private firms are reluctant to invest, and consumers are reluctant to spend, in a weak economic environment.

4. It argued that the UK had too much debt. But the UK government started the crisis with close to its lowest net public debt relative to gross domestic product in three hundred years. It still has a debt ratio much lower than its long-term historical average (which is about 110 percent of GDP).

5. The government argued that the UK could not afford additional debt. But that, of course, depends on the cost of debt. When debt is as cheap as it is today, the UK can hardly afford not to borrow. It is impossible to believe that the country cannot find public investments—the cautious IMF itself urges more spending on infrastructure—that will generate positive real returns. Indeed, with real interest rates negative, borrowing is close to a “free lunch.”

6. The government now believes that the UK has very little excess capacity. But even the most pessimistic analysts believe it has some. Of course, the right policy would address both demand and supply, together. But I, for one, cannot accept that the UK is fated to produce 16 percent less than its pre-crisis trend of growth suggested. Yes, some of that output was exaggerated. There is no reason to believe so much was.

Assessment of Austerity

We, on this side of the argument, are certainly not stating that premature austerity is the only reason for weak economies: the financial crisis, the subsequent end of the era of easy credit, and the adverse shocks are crucial. But austerity has made it far more difficult than it needed to be to deal with these shocks.

Advertisement

The right approach to a crisis of this kind is to use everything: policies that strengthen the banking system; policies that increase private sector incentives to invest; expansionary monetary policies; and, last but not least, the government’s capacity to borrow and spend.

Failing to do this, in the UK, or failing to make this possible, in the eurozone, has helped cause a lamentably weak recovery that is very likely to leave long-lasting scars. It was a huge mistake. It is not too late to change course.

This Issue

July 11, 2013

A Pianist’s A–V

Hard on Obama

The Unbearable

This Issue

July 11, 2013

A Pianist’s A–V

Hard on Obama

The Unbearable

{kind=link}